A qualified distribution is a tax- and penalty-free withdrawal from a qualified retirement plan such as a 401(k) or 403(b) plan. Qualified distributions come with conditions set by the IRS, so investors don’t avoid paying taxes.

How do you avoid penalty on 401K withdrawal?

Here’s how to avoid 401(k) fees and penalties:

- Avoid the 401(k) early withdrawal penalty.

- Shop around for low-cost funds.

- Read your 401(k) fee disclosure statement.

- Don’t leave a job before you vest in the 401(k) plan.

- Directly roll over your 401(k) to a new account.

- Compare 401(k) loans to other borrowing options.

What are the rules for early withdrawal from a 401k?

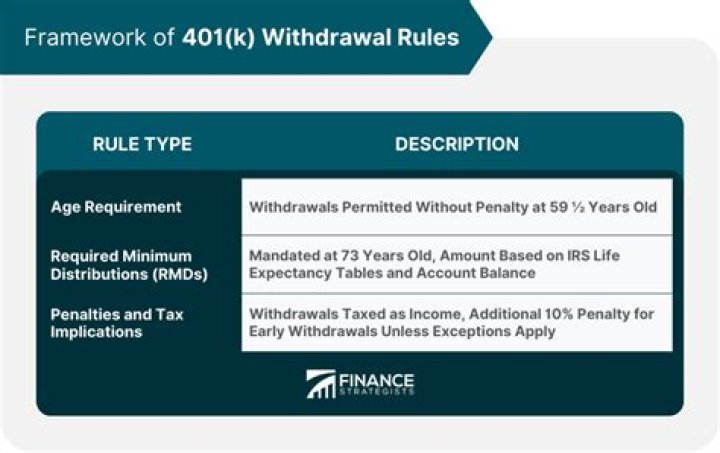

Early 401 (k) Withdrawal Rules. Early withdrawals are those taken from a 401 (k) before age 59½. They’re taxed as ordinary income, and they’re subject to an additional 10% penalty besides. But there are some exemptions from the penalty. They include total and permanent disability, loss of employment when you’re at least age 55.

Do you have to pay taxes on early withdrawal from retirement plan?

The money is taxed to the participant and is not paid back to the borrower’s account. A plan distribution before you turn 65 (or the plan’s normal retirement age, if earlier) may result in an additional income tax of 10% of the amount of the withdrawal.

When to take an early withdrawal from an IRA?

IRA withdrawals are considered early before you reach age 59½, unless you qualify for another exception to the tax. A retirement plan loan must be paid back to the borrower’s retirement account under the plan. The money is not taxed if loan meets the rules and the repayment schedule is followed.

How much can I withdraw from my 401k tax free?

You can withdraw up to $5,000 tax-free to cover costs associated with a birth or adoption. Following the March 2020 passage of the COVID-19 focused CARES ACT, it is possible to withdraw up to $100,000 from a 401 (k) early without triggering the normal 10% penalty. How Much Tax Do I Pay on a 401 (k) Withdrawal?